Prevent Bookkeeper Fraud: Biz Safety

Prevent Bookkeeper Fraud: Biz Safety

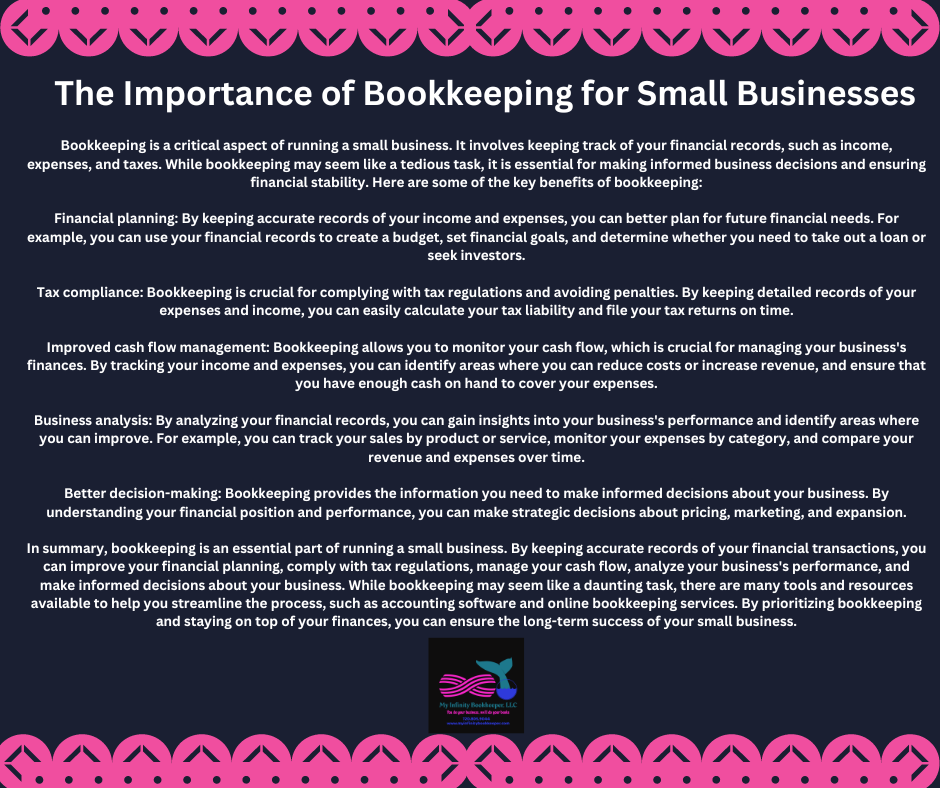

In recent news, there seems to be an alarming rise in cases of bookkeeper embezzlement and fraud. As a small business owner, the trust you place in your financial professionals is paramount. But how can you safeguard your business from these risks? It’s crucial to understand how to prevent bookkeeper fraud and implement practical steps to protect your hard-earned assets.

Understanding the Risks:

Common methods of bookkeeper fraud include unauthorized transactions and falsified records. These actions can have a devastating impact on small businesses, often leading to significant financial losses and even closure. Many business owners are unaware of the subtle ways a trusted bookkeeper can manipulate financial records, making it essential to proactively learn how to prevent bookkeeper fraud.

How do they do this? Here are just a few of the ways:

- Unauthorized Transactions:

- Transferring funds to personal accounts or accounts of shell companies.

- Making unauthorized online payments or wire transfers.

- Using company credit cards for personal expenses.

- Falsifying Records:

- Creating fake invoices or bills to justify fraudulent payments.

- Altering or deleting financial records to conceal theft.

- Manipulating payroll records to pay themselves or accomplices extra.

- Creating ghost vendors.

- Check Fraud:

-

- Forging signatures on checks.

- Altering the payee or amount on checks.

- Writing checks to themselves or accomplices.

- Payroll Fraud:

- Adding ghost employees to the payroll.

- Overstating hours worked.

- Failing to pay payroll taxes.

- Misappropriation of Funds:

- Skimming cash from sales or receipts.

- Diverting customer payments to personal accounts.

- Using company funds for personal investments.

- Expense Reimbursement Fraud:

- Submitting fake expense reports.

- Inflating expenses.

- Submitting duplicate expense reports.

What can business owners do to prevent bookkeeper fraud?

As you can see from the list above, dishonest bookkeepers can commit fraud through various methods, such as unauthorized transactions and falsified records without internal controls in place. Preventing this type of fraud requires a collective effort, as discussed in CAQ’s blog post, Fighting Fraud: A Shared Responsibility, analyzing the ACFE’s Occupational Fraud 2024: A Report to the Nations, which provides detailed statistics of occupational fraud from their study. These alarming statistics highlight the importance of multiple safeguards that every business should implement. Let’s explore practical strategies to protect your business.

Strengthening Internal Controls: Segregation of Duties

One of the most effective ways to prevent bookkeeper fraud is to implement segregation of duties. In a small business, this means separating key financial responsibilities among different individuals, or implementing systems to create the same effect. For example, ensure that the person who approves payments is not the same person who reconciles bank statements or records transactions. If you are a very small business, and have limited employees, utilize the read only access to bank accounts, and require approvals prior to any payments being made. This creates a system of checks and balances, making it more difficult for any single person to manipulate financial records undetected.

How My Infinity Bookkeeper Implements Segregation of Duties:

At My Infinity Bookkeeper, we prioritize financial security by adhering to strict segregation of duties. We operate with read-only access to our clients’ bank accounts, and all bill payments require explicit client approval. This ensures that we can accurately manage your books without having direct access to your funds, providing an added layer of protection for your business.

Implementing Regular Audits

Regular audits are essential for maintaining financial integrity and detecting potential fraud. There are two main types of audits: internal and external. Internal audits are conducted by employees or designated personnel within the company, focusing on evaluating the effectiveness of internal controls and identifying areas for improvement. External audits, on the other hand, are performed by independent certified public accountants (CPAs) who provide an unbiased assessment of the company’s financial statements.

For small businesses, it’s recommended to conduct internal audits at least quarterly, focusing on key areas like bank reconciliations, expense reports, and payroll. External audits may be less frequent, perhaps annually or bi-annually, depending on the size and complexity of the business.

How My Infinity Bookkeeper supports your audit process:

We provide detailed monthly financial reports, which act as a form of ongoing internal audit. We also assist clients in preparing for external audits by ensuring their records are accurate and organized, streamlining the audit process and minimizing potential disruptions.

Utilizing Technology for Security

Modern accounting software offers powerful features that can significantly enhance financial security and help prevent bookkeeper fraud. Look for software with robust audit trails, which track every transaction and user action, providing a clear record of who did what and when. User permission settings are also crucial, allowing you to control who has access to sensitive financial data and restrict certain actions. For example, you can grant read-only access to some users while limiting others to data entry or payment approvals.

Cloud-based accounting software adds another layer of security by providing automatic backups and encryption, protecting your data from unauthorized access.

How My Infinity Bookkeeper leverages technology for security:

My Infinity Bookkeeper leverages advanced cloud-based accounting software (like QuickBooks Online) that incorporates these security features. We ensure that our clients’ data is secure and accessible, with clear audit trails and customizable user permissions. We also stay up-to-date on the latest software updates and security patches, providing our clients with peace of mind knowing their financial information is protected by cutting-edge technology. Furthermore, we utilize the ‘close the books’ feature after each accounting period. This prevents retroactive changes to financial data, ensuring the integrity of your records and making it easier to detect any potential discrepancies.

Conclusion:

Protecting your business from bookkeeper fraud requires a proactive and multi-faceted approach. By implementing strong internal controls, conducting regular audits, and leveraging technology effectively, you can significantly reduce your risk. Remember, trust is important, but verification is essential. Taking these steps not only safeguards your finances but also provides peace of mind, allowing you to focus on growing your business with confidence.

Don’t leave your business vulnerable to financial fraud. If you’re concerned about your current bookkeeping practices or want to implement stronger safeguards, My Infinity Bookkeeper is here to help. Contact us today for a confidential consultation. We can assess your specific needs, recommend tailored solutions, and ensure your financial records are secure. Let us partner with you to prevent bookkeeper fraud and protect your business’s future.

But fear not, because I’ve got some advice to help you avoid these headaches and keep your business running smoothly.

But fear not, because I’ve got some advice to help you avoid these headaches and keep your business running smoothly.

Get your invoicing game on point: Send out those invoices promptly and make sure they clearly state the payment terms and due dates. Be confident, yet polite, when following up on outstanding payments.

Get your invoicing game on point: Send out those invoices promptly and make sure they clearly state the payment terms and due dates. Be confident, yet polite, when following up on outstanding payments.

Automate reminders: Set up automated reminders for your clients as the due date approaches. A friendly nudge can work wonders and keep everyone on track.

Automate reminders: Set up automated reminders for your clients as the due date approaches. A friendly nudge can work wonders and keep everyone on track.

Build strong relationships: Maintaining open lines of communication with your clients can help prevent misunderstandings and ensure everyone is on the same page. Plus, it’s a great opportunity to show off your amazing personality!

Build strong relationships: Maintaining open lines of communication with your clients can help prevent misunderstandings and ensure everyone is on the same page. Plus, it’s a great opportunity to show off your amazing personality!